As the current forbearance mortgage relief options come to an end, many are wondering if we’ll face a foreclosure crisis next year. This is understandable, especially for those who remember the housing crisis that began in 2008. The reality is, plans have been put in place through forbearance to ensure history doesn’t repeat itself. This year, homeowners are able to request 180 days of mortgage relief through forbearance. Upon expiration of that timeframe, they’re also entitled to request 180 additional days, bringing the total to 360 days of deferred payment eligibility. As forbearance expires, homeowners should stay in touch with their lender, because creating a plan for the deferred payments is a critical next step to avoiding foreclosure. There are multiple options for homeowners to pursue at this point, and with the right planning and communication with the lender, foreclosure doesn’t have to be one of them. Many homeowners are concerned that they’ll have to pay the deferred payments back in a lump sum payment at the end of forbearance. Thankfully, that’s not the case. Fannie Mae explains:

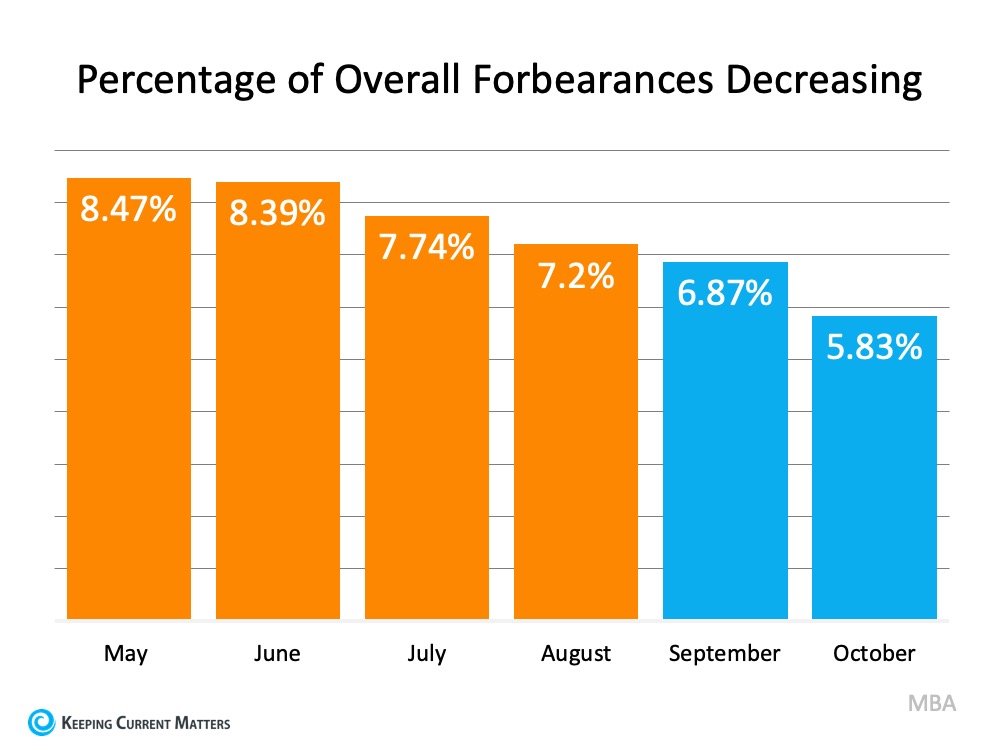

When looking at the percentage of people in forbearance, we can also see that this number has been decreasing steadily throughout the year. Fewer people than initially expected are still in forbearance, so the number of homeowners who will need to work out alternative payment options is declining (See graph below):

For those who are still in forbearance and unable to make their payments, foreclosure isn’t the only option left. In their Homeowner Equity Insights Report, CoreLogic indicates:

Many homeowners have enough equity in their homes today to be able to sell their houses instead of foreclosing. Selling and protecting the overall financial investment may be a very solid option for many homeowners. As Ivy Zelman, Founder of Zelman & Associates, mentioned in a recent podcast:

Bottom LineIf you’re currently in forbearance or think you should be because you’re concerned about being able to make your mortgage payments, reach out to your lender to discuss your options and next steps. Having a trusted and knowledgeable professional on your side to guide you is essential in this process and might be the driving factor that helps you stay in your home. The post Why the 2021 Forecast Doesn’t Call for a Foreclosure Crisis appeared first on Keeping Current Matters. from https://www.keepingcurrentmatters.com/2020/11/05/why-the-2021-forecast-doesnt-call-for-a-foreclosure-crisis/

1 Comment

6/14/2023 01:10:23 pm

Wonderful Information! Many forbearances were granted since 2020, which allowed borrowers to pause or reduce their mortgage payments for a certain amount of time. But as these are phased out, those still out of work may face new hardships. Frasco Inc has nationwide investigators who can visit properties to interview borrowers and provide current descriptions of their homes. We can also authenticate a borrower’s employment, income, assets, and public record databases. Leave a Reply. |

RSS Feed

RSS Feed